HOME BUYER TOOLKIT

FIRST, LET'S TALK ABOUT BUYING A HOME IN SAN DIEGO

As you probably know, San Diego is one of the hottest housing markets in the country... and there is probably no slowing down in the future either. In the past couple of years, we have seen historically high sales prices, with multiple offers, selling in a couple of days, and for $200k+ over the asking price. We also saw historically low-interest rates at around an average of 2.5%, which made inventory very low and created bidding wars on every home. Now we are heading back into a "normalized" market, prices went down, rates went up, and there is less competition for your favorite home.

Keep scrolling to learn more about buying your first home in SD and how my team and I can help you finally achieve your goal of homeownership!

FREQUENTLY ASKED QUESTIONS

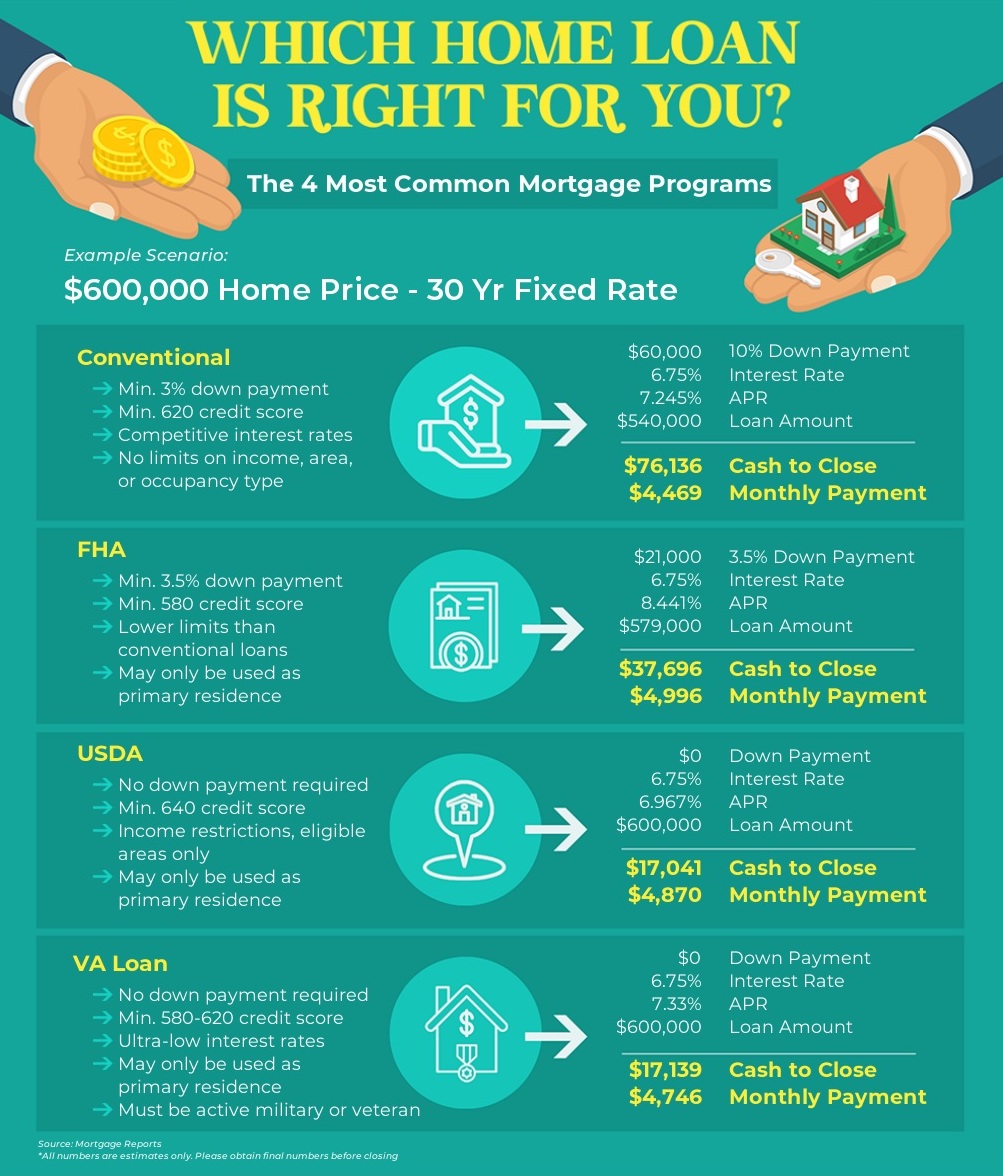

Q: Do I pay a buyer's agent a commission?

A: Nope! We are completely free to you, the sellers pay us.

Q: How big of a down payment do I need?

A: Depending on what type of loan you qualify for it could be 0-3%.

Q: What is an earnest money deposit?

A: An EMD is a deposit (usually 1-3% of the purchase price) that is given by the buyers to show their seriousness in buying the home and is held by escrow and applied towards closing costs.

Q: How much are closing costs?

A: Closing costs are the expenses over and above the property's price that buyers and sellers usually incur to complete a real estate transaction. Those costs may include loan origination fees, discount points, appraisal fees, title searches, title insurance, surveys, taxes, deed recording fees, and credit report charges. The buyer usually pays them but can negotiate to have the seller pay some or all. Closing costs are typically 1-2% of the purchase price.

Q: What is escrow?

A: Escrow is a neutral third party in a real estate transaction that holds funds until the end of the deal and reviews all documents to make sure both parties are equally protected.

Q: How long is escrow?

A: Escrow is typically around 30 days, which is the number of times buyers and sellers can get all inspections and repairs done, and when title and the lender can approve all mortgage and home buyer information/ documents. Escrow can only be 10 days during an all-cash deal.

Q: What is the MLS?

A: The Multiple Listing Service is where all the Realtors upload each home for sale, Zillow, Redfin, and all the home search websites grab those homes from the MLS.

Q: How long does a pre-approval last?

A: When a lender gives you your pre-approval letter, it will tell you how much you can afford based on your income, credit, debt, and desired monthly payments. That letter along with the price you can afford will expire usually after 60 days, which could be up to 90 in some cases.

What other questions do you have? Contact us today!

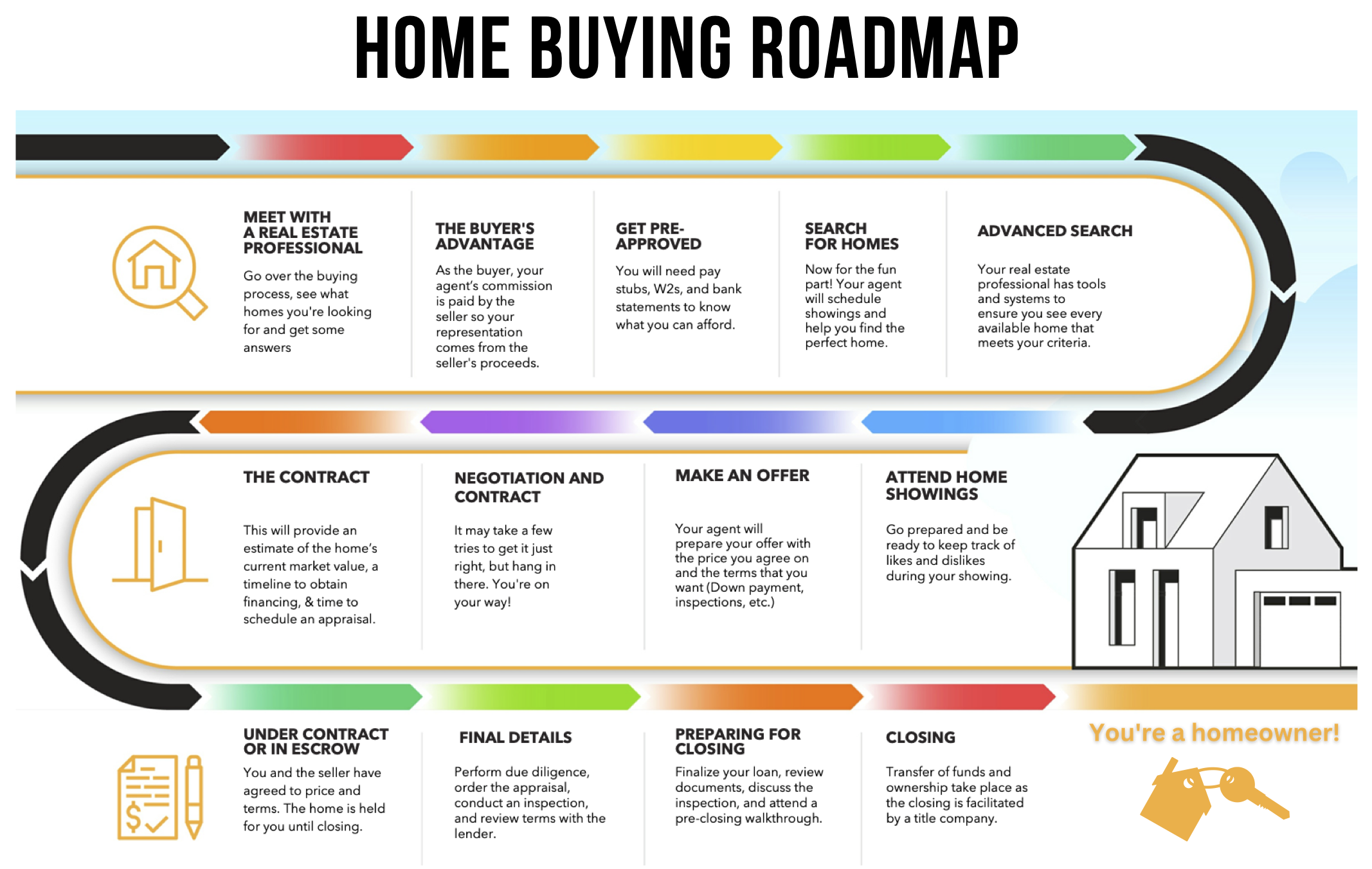

HOW TO KNOW YOU'RE READY

- Your rent is rising

- You have good credit

- Your debt is manageable

- You can afford a down payment

- You have money aside for closing costs

- You have a stable lifestyle

- You know what you want

WHAT YOU CAN AFFORD

The only way you can find out what you can afford is by speaking with a professional mortgage lender and getting pre-approved for a home loan. You'll fill out an application online and will need the following documents to do so:

- W-2 forms from the last 2 years

- Pay stubs

- Bank statements

- Tax returns from the last 2 years